Blockchain in cases of fraud and corporate insolvency

What is blockchain?

Perhaps the most concise and jargon-free definition of blockchain technology is the following:- "an incorruptible digital ledger of economic transactions that can be programmed to record not just financial transactions but virtually everything of value.”[1]

Unlike traditional financial ledgers and transactional processes, there is no requirement for a central trust authority to verify information such as the existence and ownership of assets. Instead, each transaction is verified by a majority of unrelated participants (called nodes - sometimes referred to as 'miners'). In essence, therefore, this is a democratised system. It is a peer-to-peer network whereby data is distributed amongst equally privileged nodes, each with its own copy of the ledger and predefined rules to facilitate a consensus and ensure the authenticity of the data.

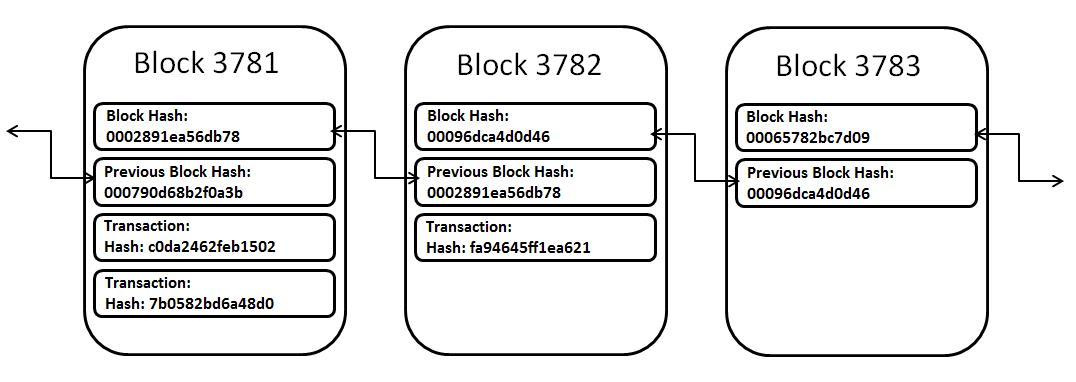

Within this framework there are both public and private networks. Public, “permissionless” blockchain ledgers allow anyone to become part of the network; Bitcoin operates on such a ledger. Private, “permissioned” ledgers might be used by a group of independent businesses for the purpose of transparent record-keeping, for instance, between a manufacturer, suppliers and distributors. The below image is a useful illustration of how information is recorded on a blockchain.

Each block contains cryptographically 'hashed' data (a digital fingerprint) and is built upon the previous block in the chain - this renders the blockchain indelible. Every block of the chain contains the hash of the previous block, and the 'append-only' nature of the database means it is impossible to modify any of the data on a block without changing the entire chain.

Each time a node seeks to add a new block to the ledger, all users must authenticate the block using a common protocol. Typically, nodes will reach a consensus regarding the validity of a new block using either the 'proof-of-work' or 'proof-of-stake' consensus algorithm[2]. If the block is valid, the nodes will add it to blockchain.

The potential uses of blockchain

Distributed Ledger Technology such as blockchain has the potential to revolutionise how the world functions on a day-to-day basis, much as the internet did from circa 1993 onwards. The financial services sector, in particular, is ripe for change in a number of ways. We explore some of the possibilities below.

Economic transactions: Verification, execution & recording

Aside from the use of cryptocurrencies as a means of making global payments cheaper and easier, we are now seeing DLT being adopted by an increasing number of financial institutions, for example:

- Mastercard launched its own blockchain network to facilitate cross-border payment of fiat currencies (such as Euros or US dollars) between banks and merchants;

- Visa's B2B Connect platform uses IBM's Hyperledger Fabric blockchain for business-to-business payments;

- JP Morgan has created a digital coin (JPM Coin) which operates privately for the purpose of facilitating money transfers between institutional accounts. The JPM coin will be issued on a blockchain network called Quorum (and subsequently operable on all standard blockchain networks), which requires permissions from JP Morgan; and

- Northern Trust recently used its Guernsey-based private equity blockchain (also using IBM's Hyperledger) to process the first live capital call using DLT for Emerald Cleantech Fund III LP. This allows investors to negotiate, review and digitally execute contracts in a manner which provides increased transparency, security and efficiency.

Investment and fund managers could also see significant benefits by utilising blockchain technology. The standard settlement time for many investment vehicles is two days, meaning that transactions may complete at a different rate than envisaged and funds are unavailable to any party while the transaction is being cleared. However, transactions can complete on a blockchain in near-real time, which results in an increased liquidity of assets with which a manager can transact. With perpetually moving markets, the ability to immediately reinvest liquid funds could be key to achieving higher returns for investors.

Tokenisation could also alleviate liquidity issues. Digital tokens can represent tangible or intangible illiquid assets (such as real property, art or intellectual property) and be used as tender for trading on the blockchain. A practical example of this is the way Ripple uses XRP (its digital currency) to transfer value from one user to another. This means that fiat currency can be displayed by a user at one end, converted into XRP and traded through RippleNet (an open-source ledger) where it is then converted it into (possibly a different) fiat currency and deposited with the recipient. This facilitates a much quicker and cost-effective currency conversion than would occur through conventional channels, ultimately making traditionally illiquid assets more liquid.

Many tasks conducted by 'middlemen' can also be expedited or negated. For instance, there will be no need for administrators to independently verify the existence and value of assets held in a fund by reference to emails and spread sheets. Instead, this will all be done by the participating nodes with a permanent record built into the blockchain, making administration much quicker and more cost effective.

Finally, data security is a particularly prevalent concern for businesses at present, and the use blockchain technology could significantly reduce the risk of a data breach. This is because all data is encrypted and distributed to participants on the blockchain, as opposed to being stored on a single, central database that might fall victim to a cyber-attack.[3]

Fraud prevention & asset tracing

With financial transactions being securely and transparently recorded to an immutable ledger with a robust verification process, asset-tracing has the potential to be much more straight-forward than is presently the case. Applying the technological capabilities to real-world cases assists in providing insight as to how fraud could be prevented and asset tracing simplified.

- Bernard Madoff was convicted of securities fraud in 2009, having engineered a pyramid investment scheme whereby early investors took money (falsely categorised as profits) at the expense of new entrants. Investors are estimated to have lost up to $65bn and the asset tracing exercise is still being conducted. Had smart contracts been available and adopted at the time, there could have been enhanced auditability and transparency, with pre-determined rules and parameters of the fund set out in unalterable code and adhered to by the participating (and incentivised) nodes. This would mean that the assets could only be invested according to those predefined rules, thereby making it almost impossible to claim title to an asset or to dispense with an asset in a manner which is not in accordance with the established protocol.

- In the case of Enron, Arthur Anderson was supposed to act a gatekeeper in verifying the accounts and protecting investors. This proved not to be the case, and the firm was found guilty of obstruction of justice after shredding thousands of audit documents. Using distributed ledger technology and smart contracts, this auditing process becomes much cheaper, quicker and more transparent. If the data were recorded to a public ledger, the transactions would be publicly visible to participants and any fraud would quickly be detected. If a permissioned network were to be used, the company could restrict the participants and their capacity. With certain blockchain technology, for instance, participants would be issued with cryptographic identity cards to enable viewing of all/some transactions. However, even such credentialed users would be unable to add to the blockchain without consensus, meaning that the majority of participants would need to conspire to commit fraud. In either case, the encrypted information would remain indelible and the parties involved identifiable, meaning anyone attempting to commit fraud would have nowhere to hide.

While the anonymity/ pseudonymity of most cryptocurrencies raises concerns about the potential for its misuse (such as terrorist financing and money laundering) this does not mean that users of cryptocurrencies are untraceable.[4] Indeed, where cryptocurrency exchanges are used to store payments and effect transactions, disclosure may be sought from those exchanges of such information as personal details, wallets, Bitcoin addresses and transaction IDs to assist in the tracing of digital assets. This will be particularly relevant with the introduction of the 5th EU Anti-Money Laundering Directive.

Blockchain technology cannot prevent fraud - ultimately it will depend upon the integrity of the participants - but it can make it much more difficult to commit and remain undetected.

Corporate insolvencies

Conducting company administrations and liquidations can be extremely challenging and time-consuming (usually at the expense of creditors). Blockchain technology could have a significant impact in this area by simplifying the insolvency process and improving returns to creditors.

In the first instance, determining whether a company is in fact insolvent ought to be an abridged process - (in Guernsey, a company fails the solvency test if it is unable to pay its debts as and when they fall due (cash flow test) or its liabilities exceed its assets (balance sheet test). With an incorruptible digital record of all transactions, those applying to place a company into administration or liquidation may be able to more easily adduce legitimate and compelling evidence to a court of a company's financial status.

Proving creditor claims may become much more manageable. The evidentiary trail of transactions entered into between companies and purported creditors will be accessible on the blockchain. This could negate the need for creditors to provide documentary evidence of their debt (which may or may not still exist).

Retention of title claims may also be more straightforward to evidence using blockchain ledgers. With the use of smart contracts, a particular asset can be digitally tagged as belonging to the seller until such time as a specified condition is met. If that condition (e.g. payment) is not fulfilled, it will be clear that the asset still belongs to the seller. This digital mark will be visible to potential successive recipients of the asset and to the respective nodes seeking to validate any subsequent transaction, meaning that the asset would not be sold on to a third party where title remains with the seller.

Company directors owe duties to the company they serve and the company legislation creates potential personal liability for certain actions such as trading whilst insolvent. If board decisions (and the reasons for taking them) are recorded on the blockchain (e.g. using Boardroom[5]) then evidencing allegations (for the IP) or defending them (for the board) will be far easier, as may be evidencing the critical time when the company became insolvent (as set out above). That said, the paramount need to keep accurate and thorough records remains, however those records are stored.

Conclusion

There is some way to go before blockchain technology completely revolutionises the financial services sector, but we are seeing a gradual increase in its uptake.

It is inevitable that Distributed Ledger Technology will play an increasingly significant role in global industry, but the financial services sector in particular is likely to see a paradigm shift in the coming years. With the possibility of providing financial services to the underbanked and unbanked, the ability to expedite economic transactions at a significantly reduced cost and the potential to become a near-cashless society with the use of cryptocurrencies and digital tokens, it is time for the financial services sector to embrace the change and develop a long-term strategy for the use of DLT in an imminently-regulated environment.

------------------------------------------

[1] Don & Alex Tapscott, authors Blockchain Revolution: How the technology behind Bitcoin is changing money, business and the world (2016).

[2] Proof-of-work requires that the nodes provide significant computer power to participate in the validation process, whereas proof-of-stake participation is contingent upon the amount of a specific cryptocurrency held by the respective node.

[3] Although concerns have been raised that an immutable ledger is contrary to the right to be forgotten, or the right to rectification of data.

[4] There are exceptions, such as Monero, which asserts that its cryptography facilitates entirely untraceable transactions.

An original version of this article was published by Compliance Matters, June 2019.

© Carey Olsen 2019.