Expansion of Private Investment Fund (PIF) regime

The Guernsey Financial Services Commission (“GFSC”) has announced the addition of two new types of Private Investment Fund (“PIF”) to its regulatory stable, pursuant to the Private Investment Fund Rules 2021 (the “Rules”). The existing PIF will continue to be available.

PIFs were introduced by the GFSC in 2016 as a simple and quick to market private Guernsey fund.

PIFs have their regulatory registration issued in one business day by the GFSC and there are no requirements for full information particulars (such as a prospectus) to be prepared or submitted to the GFSC.

The different types of PIF available are as follows.

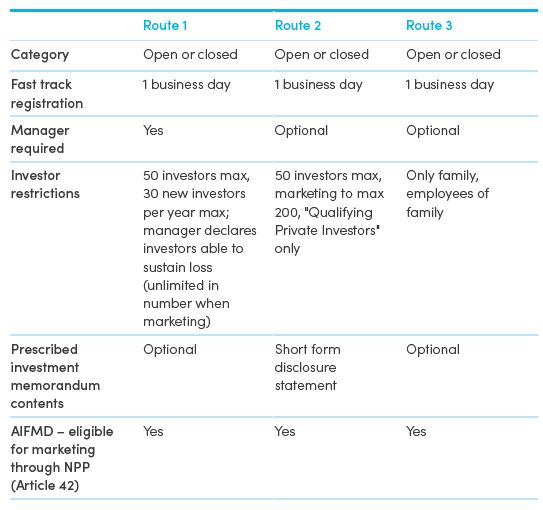

Route 1 - POI Licensed Manager PIFs (the pre-existing regime)

The “POI Licensed Manager” PIF is suited to fund managers that have a closer relationship with their investors. Its distinguishing features include no requirement for minimum investment, a maximum of 50 legal or natural persons holding an economic interest (with no more than 30 admitted in a 12 month period) and no limit imposed on the number of potential investors that the fund can be marketed to.

A Route 1 PIF must appoint a Guernsey licensed manager, with the manager being responsible at the time of application to make declarations to the GFSC on the investors’ ability to suffer loss.

The new regime

The new regime introduces two new categories of PIFs that (like all Guernsey funds), must appoint a designated administrator, but unlike Route 1 are not required (though may still elect) to appoint a locally licenced manager.

Route 2 - Qualifying Private Investor PIFs

A “Qualifying Private Investor” PIF is available to investors who can evaluate the risks and strategy of investing in a PIF and bear the consequences of investment, including the possibility of any loss arising from the investment. The Rules contain related definitions of “Professional Investor”, “Experienced Investor” and “Knowledgeable Employee” as to how an investor can be categorised as a Qualifying Professional Investor.

Qualifying Private Investor PIFs are also subject to a maximum of 50 legal or natural persons holding an economic interest in the fund. Marketing can take place to a maximum of 200 people. Investors must be provided with a disclosure statement that states all material information (including risk disclosures) that an investor would reasonably require to make an informed judgement about the merits and risks of investing in the PIF, as well as certain prescribed disclosures.

The administrator must make a declaration to the GFSC that effective procedures are in place to restrict the fund to Qualifying Professional Investors. The administrator should also receive written acknowledgement of receipt of the above mentioned disclosure statement from investors.

Route 3 - Family Relationship PIFs

A “Family Relationship” PIF is available to investors who share a family relationship or are an employee of the family. The Family Relationship PIF cannot be marketed outside the family group.

The administrator must make a declaration to the GFSC that effective procedures are in place to ensure that all investors fulfil the requirement of being related as a family.

Carey Olsen comment

The GFSC has responded to industry and investor sentiment that the scope of the already extremely popular PIF product could be extended. We anticipate the streamlining of PIFs into three routes will be very attractive to fund managers for the inherent flexibility.

As a reminder, if there is a licensed manager in a PIF structure, a business risk assessment must be submitted in respect of such manager, but no rules apply to the manager.

As with all Guernsey fund structures, the key individuals behind the promoter of the fund submit forms OPQ to the GFSC, as do key persons involved in the manager (if any) and if the fund is a company, each director.

This table summarises the different PIF Routes.

Legal Team法律团队

Annette Alexander

Annette Alexander

+44 (0)1481 732067

Email Annette

电邮 Annette Alexander

Christopher Anderson

Christopher Anderson

+44 (0)1481 741537

Email Christopher

电邮 Christopher Anderson

Andrew Boyce

Andrew Boyce

+44 (0)1481 732078

Email Andrew

电邮 Andrew Boyce

Matthew Brehaut

Matthew Brehaut

+44 (0)20 7614 5620

Email Matthew

电邮 Matthew Brehaut

Tom Carey

Tom Carey

+44 (0)1481 741559

Email Tom

电邮 Tom Carey

David Crosland

David Crosland

+44 (0)1481 741556

Email David

电邮 David Crosland

Tony Lane

Tony Lane

+44 (0)1481 732086

Email Tony

电邮 Tony Lane