Bridge Finance and Litigation Funding Structure Analysis

Definitions:

"LCF Law" means The Lending, Credit and Finance (Bailiwick of Guernsey) Law, 2022.

"Notice" means the Guernsey Financial Services Commission's Notice with respect to the disapplication of the requirement to hold a licence under section 40 of the Lending, Credit and Finance (Bailiwick of Guernsey) Law, 2022.

-

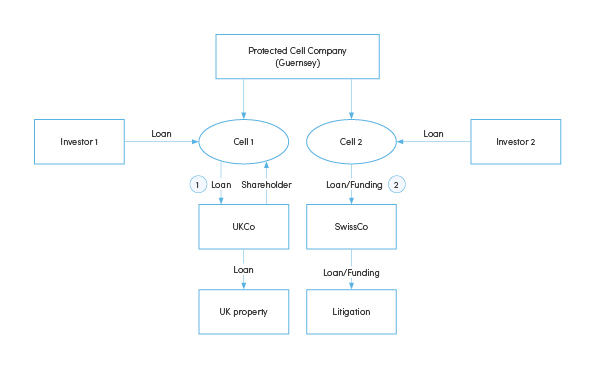

Cell 1 sitting between the investor and the UK bridge finance provider

The loan might be subject to Part III of the LCF Law, as "lending" (and thereby constituting the Cell as a "financial firm business").

However, the requirement for Cell 1 to hold a licence under Part III of the LCF Law is disapplied under paragraph III of the second section of the Notice, which exempts "Persons who carry out lending to their registered directors, registered partners, registered shareholders, or beneficial owners."

Note that unlike the equivalent exemption in respect of Part II, there is no need that the shareholder be a bona fide shareholder, as is the case for the equivalent exemption in respect of Part II of the LCF Law.

Consideration should also be given to Cell 1's intermediation activities, which would require a Part IV Licence.

The question is whether Cell 1 is providing "alternative non-bank credit or finance intermediation".

Under the LCF Law, "alternative non-bank credit or finance intermediation" means "intermediation or brokerage services, whether or not provided by electronic means, for the purposes of matching lenders with borrowers."

We do not consider that there is any "matching" here since the structure is being put in place by agreement of Investor 1 and UK Co.

Accordingly, we do not think this falls within the scope of Part IV of the LCF Law.

-

Cell 2 lending to fund litigation

The loan might be subject to Part III of the LCF Law, as "lending" (and thereby constituting the Cell as a "financial firm business").

However, on the assumption that the loan / funding is true "litigation funding", in that Cell 2 is taking the risk of the litigation being successful / failing, we do not consider that this constitutes "lending" (or any other financial firm business).

On the basis that this is not "lending", we also do not consider that Cell 2 is providing "alternative non-bank credit or finance intermediation".

Legal Team法律团队

Related

有关

A guide to the Lending, Credit and Finance (Bailiwick Of Guernsey) Law, 2022

Part II: Consumer credit and home finance

Part II: Unfair contract terms

Part III: Financial firm business

Part III: Virtual asset service providers

Part IV: Financial platforms and intermediation

Discretionary exemptions

Part II Licence Decision Tree

Part III FFB Licence Decision Tree

Part III VASP Licence Decision Tree

Part IV Licence Decision Tree

Private Equity Structure Analysis

Trust Structure Analysis

Family Loan Structure Analysis